There’s a lot to unpack in the real estate market right now, but for potential homebuyers, the coming months could be an exciting time. Let’s dive into two key trends that are pointing towards a more favorable market for buyers.

Inflation and Mortgage Rate Outlook

First, there’s some positive news on the inflation front for mortgage rates. The most recent CPI inflation report showed that inflation decreased on a month-over-month basis, which was the first time since 2020. This is a significant development, as inflation has been a major driver of rising interest rates over the last few years. A continued dip in inflation is likely paving the way for a rate cut by the Federal Open Market Committee (FOMC) to the Fed Funds Rate later this fall. In fact, the markets are currently pricing in a probability of over 90% that we will see a rate cut following the September FOMC meeting, which will help bring down mortgage rates. This will help make homeownership more affordable and bring about refinancing opportunities for current homeowners.

Housing Inventory Increasing

On the housing market side, we continue to see inventory build for both existing and newly constructed homes. Although lower mortgage rates will allow for more buyers to enter the market, more homes also mean more options for you to find your perfect fit. Whether you’re looking for a cozy starter home or a spacious family residence, the growing inventory expands your choices and reduces the pressure often felt in a low inventory market.

What does this mean for homebuyers?

If you’ve been thinking about buying a home, these trends could be a sign that the time is right. With potentially lower mortgage rates and a shift in the housing market, you may be able to find a great home at a good price.

Here are some steps you can take to get ahead of the curve:

Get pre-approved for a mortgage. This will give you a clear understanding of how much you can afford to borrow and make you a more competitive buyer.

Start your house hunt early. With a potential for lower rates in the future, the sooner you start looking, the better chance you’ll have of finding your dream home before competition increases.

Work with a real estate agent. A real estate agent professional can help you navigate the buying process, negotiate offers, and find the right home for your needs.

The housing market may be shifting, but with the right preparation and a little guidance, you can turn this shift into an opportunity to achieve your homeownership goals. Let’s get you started on your journey today!

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

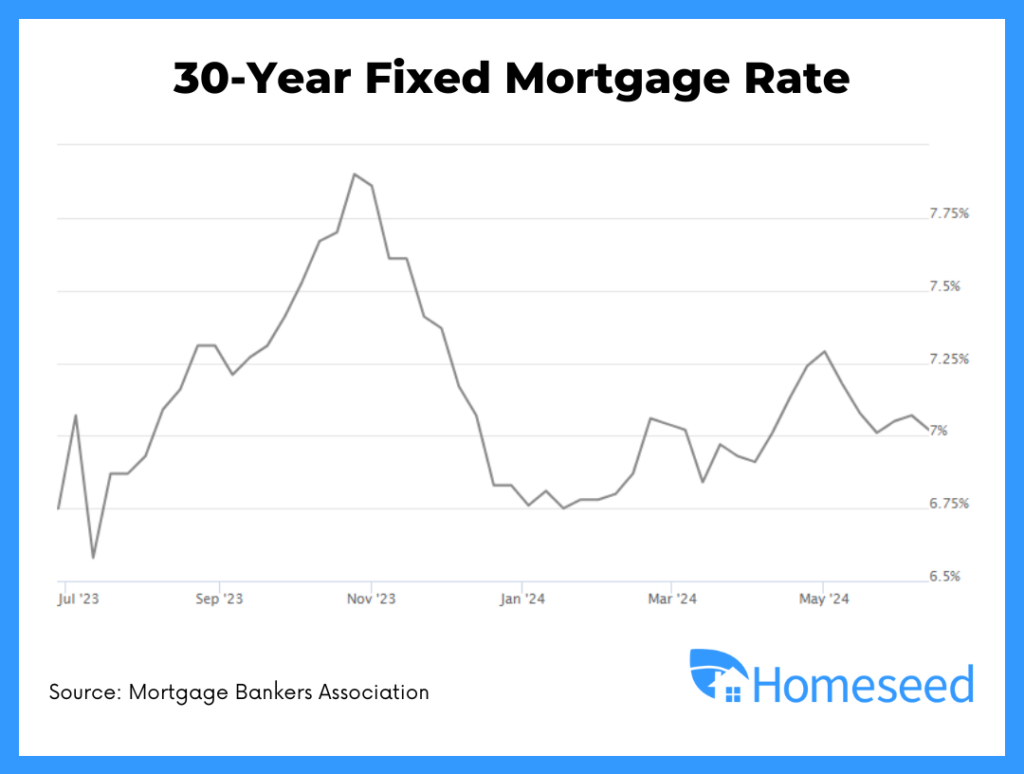

Mortgage rates are slightly lower on a week-over-week basis and have been fluctuating within a narrow range over the last month.

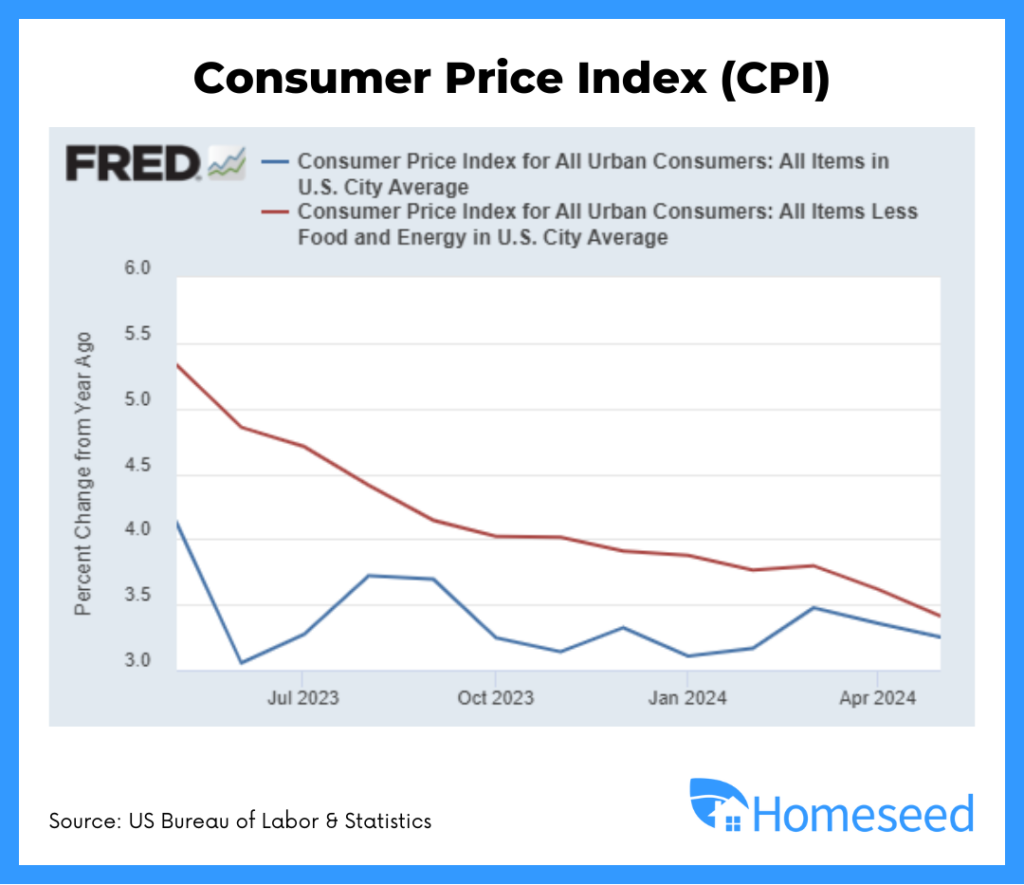

Expectations are for tomorrow’s CPI report to show year-over-year inflation decreasing from 3.3% to 3.1%, which would be good for mortgage rates.

Market futures are showing two potential rate cuts by the end of 2024 as having the highest probability.

Consumer Price Index

Headline inflation fell from 3.3% to 3.0% year-over-year,

June CPI showed a large moderation in the shelter component.

There is a long lag in reflecting real world market conditions, but we continue this trend in shelter inflation lowering.

BLS Jobs Report

June’s job growth was slightly above estimates with a reported 206,000 new jobs created.

However, there were big revisions to the two previous months with a combined 111K jobs removed.

Unemployment also rose to 4.1%, which triggered a reliable economic indicator suggesting we are already in a recession.

Digging Deeper on Housing Inventory and Prices

Active inventory has risen 6.7% in June and is up 37% year-over-year, but this is from very low numbers with one third of the increase coming from two states alone – Florida and Texas.

On the moderation of median home prices, this is skewed by the mix of sales (lower priced homes are selling more than higher priced homes), which brings down the median price sold.

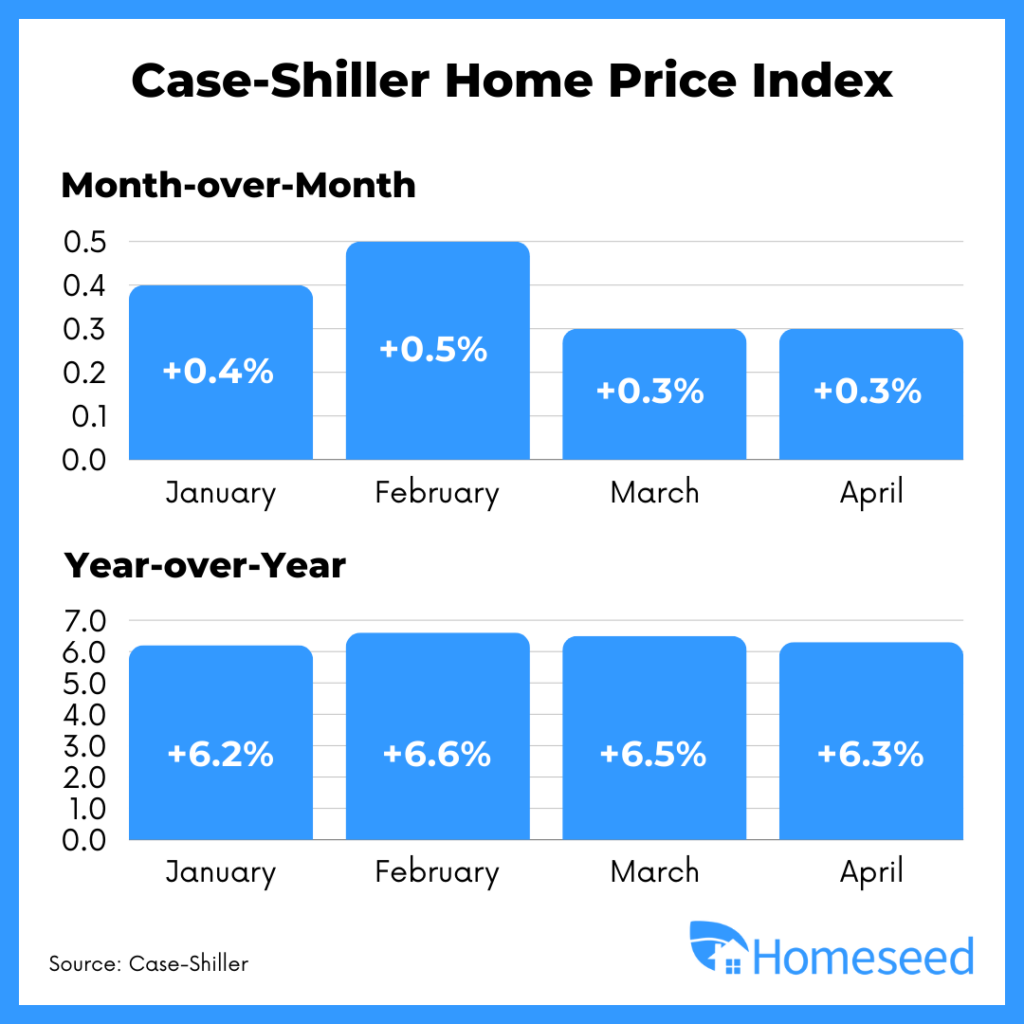

Home values across the board are increasing as shown in the recent Case-Shiller Home Price Index and inventory remains much lower than pre-pandemic levels.

RATES EDGE SLIGHTLY UNDER 7% – Mortgage rates average just under 7% for top tier scenarios according to this index. https://www.mortgagenewsdaily.com/…

WHEN WILL RATE CUTS COME – The Fed says it needs greater confidence inflation is moving towards its 2% goal before they will cut rates. https://www.cnbc.com/…

AFFORDABILITY CHALLENGES – How getting inflation back towards the Fed’s 2% target will help housing. https://www.housingwire.com/…

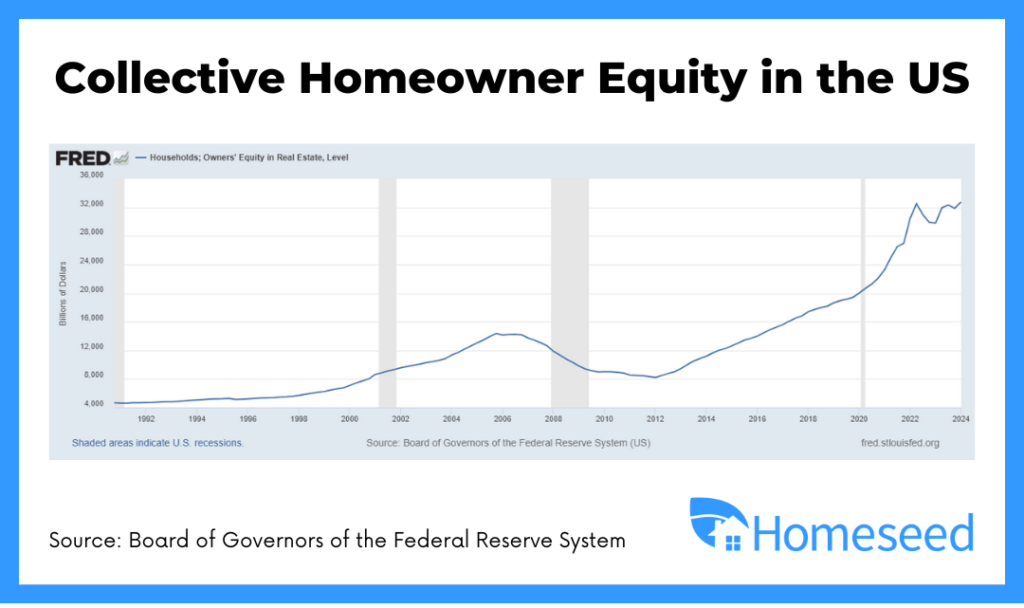

Homeowners across the country are experiencing unprecedented levels of home equity as home values continue to rise. This surge presents a unique opportunity to leverage that equity through a cash-out refinance. In this blog post, we’ll explore what a cash-out refinance is, how it works, and how it can be a strategic move for consolidating debt and funding significant investments or projects.

What is a Cash-Out Refinance?

A cash-out refinance is a financial transaction in which you replace your existing mortgage with a new one that’s larger than what you currently owe. The difference between the new loan amount and the existing mortgage balance is paid out to you in cash. Here’s a simple breakdown of how it works:

Appraisal: Your home’s value is assessed to determine how much equity you have.

New Mortgage: You take out a new mortgage for more than you owe on your current one, limited up to 80% of the current appraised value.

Cash Payment: You receive the difference in cash, which can be used for a variety of purposes.

Consolidating Your Debts

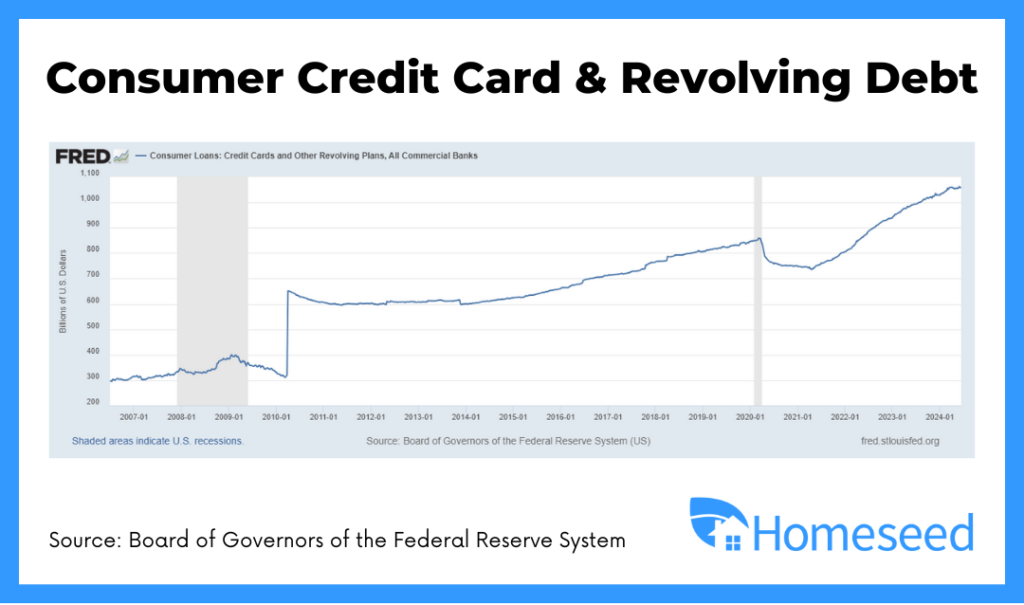

Alongside rising home equity, debt levels have also reached new heights. Many homeowners carry high-interest debt from credit cards, personal loans, or other sources. A cash-out refinance can be an effective tool for consolidating this debt. By using the cash from the refinance to pay off high-interest debts, you can lower your overall monthly payments and improve your cash flow.

Lowering Your Blended Interest Rate

One of the key considerations in deciding whether to pursue a cash-out refinance is the interest rates involved. Even if your current mortgage rate is lower than the rate you would get with a cash-out refinance, your overall blended interest rate—taking into account all your debts—could be lower. This means you could save money in the long run by consolidating high-interest debts into a single, more manageable payment.

Fundings for Projects or Investments

Home Improvement Projects: Invest in renovations or upgrades that can increase your home’s value even further.

Purchasing a Second Home: Use the cash to make a down payment on a vacation home or rental property.

Other Investments: Allocate funds towards other investment opportunities that can potentially yield higher returns.

Learn More About Your Options

With home equity at an all-time high and debt levels rising, a cash-out refinance offers a strategic way to manage finances, reduce debt, and fund important projects or investments. By understanding how it works and considering your financial goals, you can make informed decisions that maximize the benefits of your home’s value.

If you’re considering a cash-out refinance, contact Homeseed today to discuss your options and see how we can help you achieve your financial objectives.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are higher week-over-week despite lower inflation from the PCE report last Friday, along with weaker manufacturing data from today.

Market experts believe that bonds, which drive mortgage rates, are are reacting to concerns about a potential GOP sweep in the government, which could have negative implications for Treasury supply.

Looking ahead, we might see increased rate volatility during this election year as we approach the end of 2024.

Home Values Continue to Increase

Two of the most notable home price indices, Case-Shiller and FHFA, show that home values continue to rise on a year-over-year basis in their most recent reports.

Both Case-Shiller and FHFA reported year-over-year gains of 6.3%.

Strong demand and tight supply will likely push home values higher and allow homeowners to build wealth through equity.

Existing Home Sales

Inventory increased 6.7% month-over-month in May 2024 and is up 18.5% year-over-year.

Homes were on the market for a national average of 24 days.

Given the demand and low inventory, 30% of homes sold above the list price.

RATES MOVE HIGHER – Concerns over a potential sweep by the GOP in the upcoming elections could have negative implications for Treasury supply, which have driven up mortgage rates. https://www.mortgagenewsdaily.com/…

PERSONAL CONSUMPTION EXPENDITURES – Tomorrow’s PCE report is expected to show the lowest core reading since March 2021. https://www.cnbc.com/…

USING AI FOR APPRAISALS – The CFPB approved a new rule that aims to govern how AI is used to estimate the value of a home. https://www.housingwire.com/…

WHEN WILL HOME PRICES GO DOWN – Six economists weigh in on the likelihood of home prices going down. https://www.morningstar.com/…

Welcome to Homeseed’s Summer Market Update for 2024! As we reach the halfway point of the year, it’s essential to reflect on the trends and developments that have shaped the mortgage market and housing industry thus far. The first six months of 2024 have been characterized by fluctuating mortgage rates, evolving economic conditions, and dynamic shifts in buyer behavior. Let’s dive into the key insights and projections that will guide us through the remainder of 2024.

Factors Influencing Mortgage Rates

Federal Reserve:

Controls short-term interest rates that indirectly impacting mortgage rates.

As a general rule of thumb, rates rise in a strong economy and fall when the economy slows.

Inflation:

Bond Market: Inflation can reduce investor demand for mortgage-backed securities, which then causes bond prices to fall and mortgage rates to increase.

Devaluation of Dollar: As inflation increases, the purchasing power of the dollar decreases, which can lead to higher prices for everything, including mortgage rates.

Monthly Jobs Report:

Strong employment and wages can put upward pressure on inflation.

Weak employment data and rising unemployment will lead to rate cuts in an attempt to jumpstart the economy.

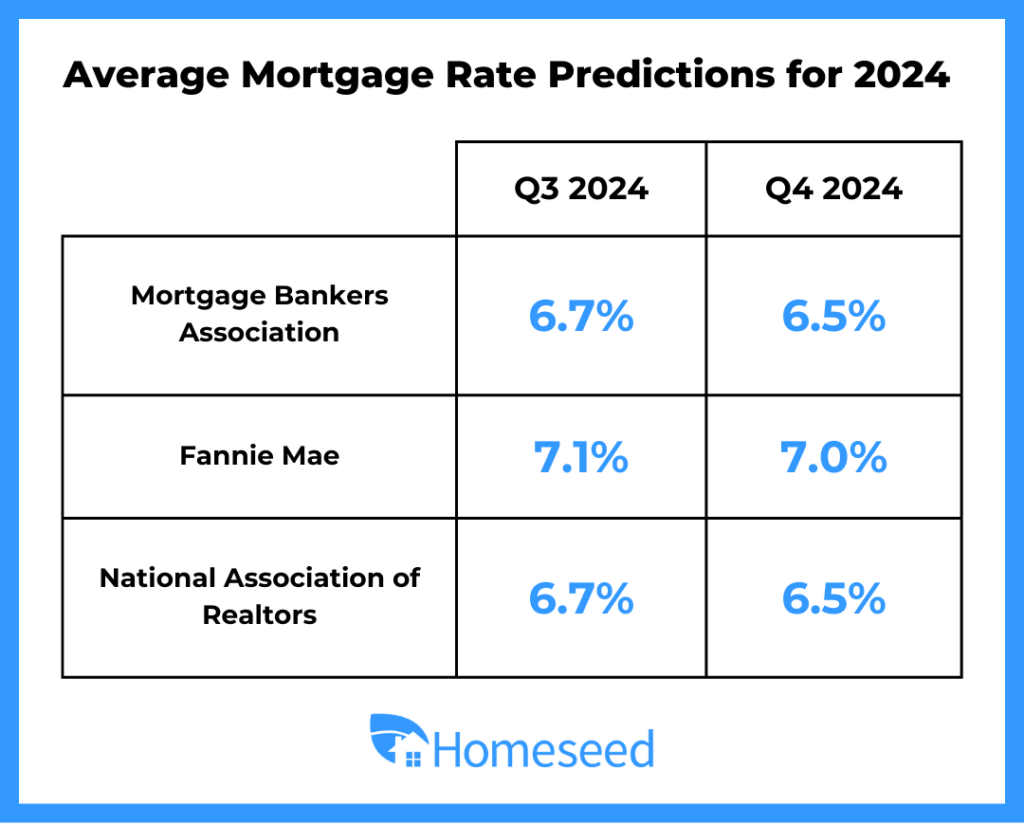

Mortgage Rate Outlook & Predictions

Initial 2024 Predictions:

Early 2024 predictions included three rate cuts by the Fed, which lead many experts in the industry to predict mortgage rates would fall in to the low 6% range by the end of the year.

Concerns that the Fed would keep rates higher for longer began to arise in the first quarter of 2024 due to stalled progress on getting inflation towards their 2% goal.

Recent FOMC Meeting:

Median expectation by Fed members now shows only one potential rate cut in 2024.

Recent economic data has shown softening inflation and labor market, leading to lower rates over the past two months.

Future Rate Trends:

Most forecasts expect mortgage rates to fall slightly towards the end of 2024 to a range of 6.5% – 6.75%.

Significant drops in inflation and rising unemployment could lead to faster rate decreases.

Key reports influencing rates: BLS Jobs Report and Consumer Price Index (CPI).

Chance of increased volatility in rates as we near the presidential election due to any potential uncertainty that may come about.

Housing Market Update

Inventory and Supply:

Inventory up nearly 35% from 2023, but still well below historical supply prior to the pandemic.

Current inventory at 3.7 months’ supply compared to what is considered a balanced market at 6 months supply.

Home Values & Demand:

Home values will likely continue to increase through the end of 2024 as demand outweighs supply.

Mortgage application volume for purchases have increased for three consecutive weeks and are at the highest level since January 2024.

Consumer Debt & Home Equity

Record High Consumer Debt:

Consumer debt reached $1.15 trillion in Q1 2024.

High credit card debt, rising charge-offs, and delinquencies suggest a potential slowdown in consumer spending.

Impact on Economy:

Reduced consumer spending could lower inflation and slow the economy, benefiting mortgage rates.

Homeowners with high equity and debt could benefit from cash-out refinancing to improve cash flow.

Opportunities This Summer

The summer market is brimming with opportunities for both homeowners and homebuyers. With potential mortgage rate adjustments expected later this year, an estimated 5 million buyers could enter the market for every 1% drop in rates. Alongside the expanding inventory, this is the perfect time to stay informed and make strategic financial decisions. Whether you’re looking to upgrade your current home or start your homeownership journey, reach out today to explore the opportunities available this summer.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

It’s been a volatile week for rates as they are now slightly lower than where they were a week ago.

A strong BLS Jobs Report earlier in the month moved rates higher before last week’s CPI report brought them back down.

Last Thursday’s Producer Price Index helped rates move even lower as inflation measured from the perspective of manufacturers came in much lower than expected.

Consumer Price Index (CPI)

The May CPI report showed that overall inflation was flat at 0% month-over-month (expected 0.1%) and decreased year-over-year from 3.4% to 3.3%.

May brought cooler than expected consumer inflation, due in large part to easing motor vehicle insurance costs.

This follows better than expected readings in April as the annual Headline and Core readings both took important steps lower.

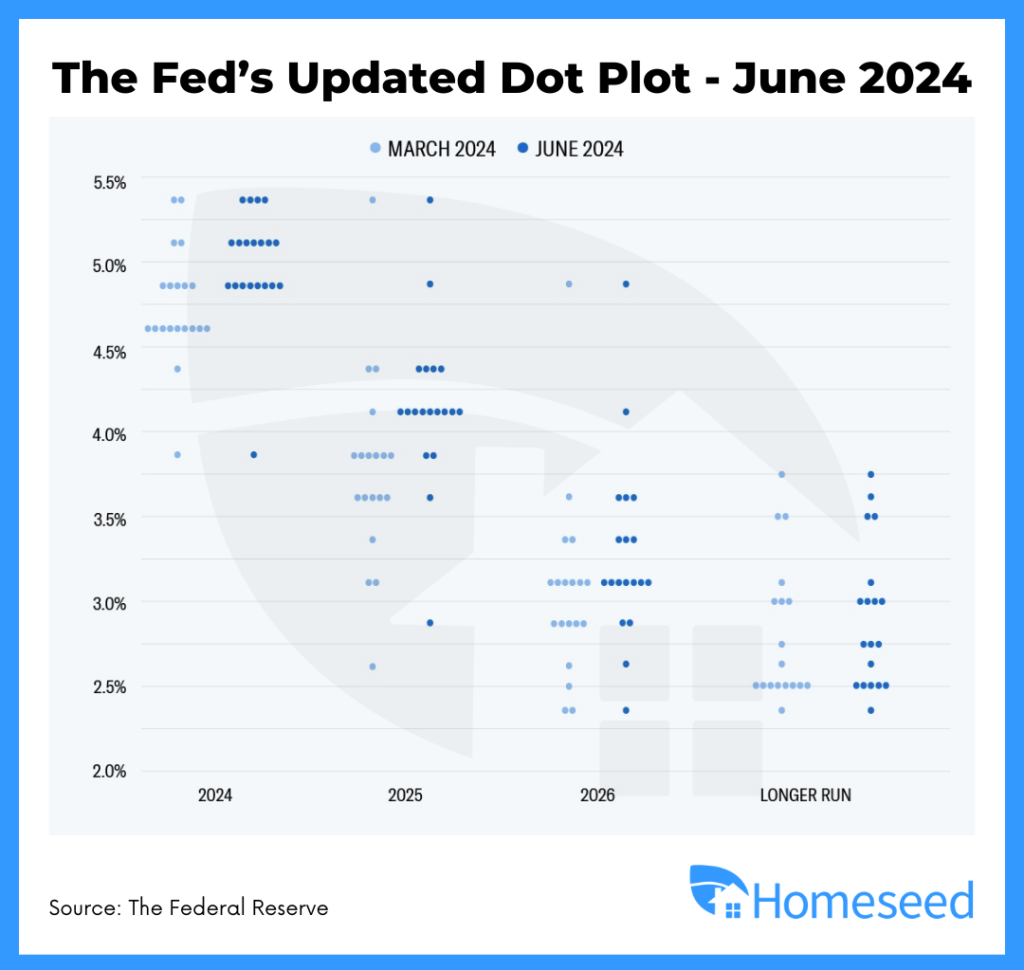

The Fed Meeting

The Fed’s fourth meeting of the year concluded last Wednesday and left their Fed Funds Rate unchanged once again.

An updated dot plot showed that the median forecast for the rest of the year would be one rate cut.

Fed Chair Jerome Powell acknowledged that their policy is restrictive but needs to see more progress on inflation lowering.

RATES DROP AFTER CPI DATA – Lower inflation numbers help bring rates back down after last week’s spike from the BLS jobs data. https://www.mortgagenewsdaily.com/…

WHOLESALE PRICES COME DOWN – The Producer Price Index (PPI), a gauge of prices that producers get for their goods and services, declined 0.2% for the month. https://www.cnbc.com/…

MORTGAGE APPLICATIONS RISE IN MAY – New-home purchase mortgage applications rose 1% month-over-month in May according to the Mortgage Bankers Association (MBA). https://www.housingwire.com/…

VA NOW ALLOWING BUYER-PAID BROKER FEES – Veterans using VA home loan benefits will have the ability to pay the buyer-broker fee beginning August 10, 2024. https://news.va.gov/…

Purchasing a home is a significant, exciting milestone that can help you build generational wealth. Whether you’re a first-time homebuyer or looking to upgrade, achieving this dream is possible, but there are several hurdles to navigate in today’s housing market. Limited housing supply and ongoing affordability challenges are common obstacles that potential homeowners must overcome. In this blog, we’ll explore various challenges that homebuyers are facing in today’s market and provide housing hacks and financing strategies to help you overcome these common challenges.

1. Buy Before You Sell

One of the biggest dilemmas for homeowners looking to upgrade is buying a new home before selling their current one. Our “Buy Before You Sell” program addresses this by allowing you to make a non-contingent offer on a new home before selling your existing property.

How It Works:

You receive financial backing to purchase your new home without needing to sell your current one first.

This enables you to make a stronger, non-contingent offer, which is often more attractive to sellers.

Benefits:

Avoid the stress of timing two transactions perfectly.

Have the comfort of moving into your new home before dealing with the sale of your old one.

2. Down Payment Assistance

Saving for a down payment can be a daunting task, especially if you have limited savings. Or perhaps you want to keep some of your savings to furnish your home after closing. Fortunately, our Homeseed 100 Program is available to help with down payments and reducing your cash-to-close, even if you’re not a first-time homebuyer. We also offer down payment assistance through the Washington State Housing Finance Commission, where there are additional programs with income restrictions that could be potentially better suited for underserved and low-income communities.

Homeseed 100 Program Highlights:

No income restrictions.

Minimum credit score of 620.

Repayable and non-repayable assistance

Up to 5% assistance for the down payment and closing costs.

Manufactured homes allowed.

2-1 interest rate buydowns available.

3. Stronger Offers with a Cash Committed Credit Approval

Homeseed’s goal is to reduce the stress of the mortgage process by helping our clients prepare early and make our clients’ offers stand out in a competitive market. To do so, we’ve developed our Cash Committed Credit Approval™ program to help achieve this. We’ll provide you with a fully underwritten credit approval for financing before you find your home so you can shop with confidence. Additionally, sellers will find your offer that much more attractive knowing that you’ll close on time or our Cash Committed Credit Approval™ program will issue a $10,000 credit to them. Please see full terms and conditions at bit.ly/homeseedccc.

How It Works:

Complete a loan application and request to enroll in our Cash Committed Credit Approval program prior to making an offer.

Respond to all of our requests on time as outlined in our terms and conditions.

We will guarantee the transaction closes on time or we will issue $10,000 to the seller.

4. Multi-Family Property Purchase

Purchasing a multi-family property offers numerous benefits, making it an attractive investment option. One of the key advantages is that potential rental income from the other units can be used when qualifying for the mortgage. For individuals looking to get into real estate investing, purchasing a multi-family property provides an opportunity to build wealth and financial stability as you live in one unit and rent out the others to offset living expenses.

Scenario: Imagine Jane, an aspiring real estate investor, decides to purchase a duplex for $800,000. She secures a mortgage with a 20% down payment of $160,000, leaving her with a loan of $640,000 at a 6% interest rate. Sarah plans to live in one unit while renting out the other.

The rental market in her area is strong, and she finds a tenant who agrees to rent the second unit for $2,000 per month. The monthly mortgage payment for her loan, including principal and interest, is approximately $3,837. Adding property taxes and insurance, her total monthly housing cost comes to about $4,500.

With the rental income of $2,000 per month, Sarah’s out-of-pocket expense for housing is reduced to $2,500 per month. This makes homeownership more affordable for her. Additionally, Sarah benefits from potential property appreciation and tax advantages such as deductions for mortgage interest, property taxes, and depreciation on the rental unit. By renting out the second unit, Sarah not only reduces her living costs but also builds equity in the property, paving the way for future investment opportunities and financial growth.

5. Funds for Investing: HELOCs

A Home Equity Line of Credit (HELOC) offers significant benefits, particularly if you are looking for a quick way to tap into your home’s equity. It provides flexible access to funds by leveraging the equity built up in your current home, allowing for the financing of a new home purchase or another investment. This flexibility can ease the stress of timing for your particular goals, offering funds that cover down payments, renovations, and much more.

HELOC Highlights:

A flexible credit line secured by your home’s equity and allows for periodic access to funds when needed.

Adjustable interest rates, providing flexibility but requiring careful financial planning.

6. Utilizing a Rent-Back Agreement When Selling

A Rent-Back agreement allows the seller to remain in the home for a specified period, paying rent to the new homeowner. It provides the seller with additional time to secure a new residence and complete their move, potentially saving time and money as they would not need to move into new temporary housing before purchasing a new home.

Scenario: Imagine John just closed the sale of their home in Seattle but needs an additional 30 days to finalize the purchase of a new property. He enters into a rent-back agreement with the buyer, agreeing to pay a monthly rent equivalent to the new homeowner’s mortgage payment, property taxes, and insurance costs. The terms are clearly outlined in a written agreement, including a refundable deposit to cover any potential damages. The buyer, now the official homeowner and temporary landlord, benefits from an additional rental income that can help offset moving and closing costs. Meanwhile, the seller enjoys the stability of remaining in their home while they transition to their new one, avoiding the inconvenience and expense of temporary housing.

Get In Touch With Your Homeseed Loan Advisor

Your Homeseed Loan Advisor is here to offer innovative solutions to common homebuying obstacles, making your path to homeownership more accessible and manageable. By leveraging strategies such as Buy Before You Sell, down payment assistance, cash committed credit approvals, HELOCs, and other creative financing ideas, you can navigate the challenges of today’s real estate market with confidence. Explore these options to take control of your homebuying journey and turn your homeownership dreams into reality.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates moved higher in the early half of last week, but have since moved back down.

April’s Personal Consumption Expenditures (PCE) report was released last Friday, which showed inflation slightly below expectations and helped rates move lower.

Today’s weaker manufacturing data further supported the decrease in rates and we essentially back to where we were for rates about a week ago.

Personal Consumptions Expenditure

The Fed’s favored inflation measure, Core PCE, rose 0.2% from March to April, coming in slightly below estimates.

On an annual basis, Core PCE remained at 2.8% for the 12 months ending in April.

While this is well below 2022’s 5.6% peak, progress toward the Fed’s 2% inflation target remains stalled.

All-Time High for Home Values

Two of the most notable home price indices, Case-Shiller and FHFA, show that home values continue to rise on a year-over-year basis in their most recent reports for the end of March 2024.

Case-Shiller reports that home prices rose 6.5% year-over-year while FHFA reported a year-over-year gain of 6.6%.

Strong demand and tight supply will continue to push home values higher and help homeowners build wealth through equity.

ERASING LAST WEEK’S SPIKE – Lower inflation and weaker manufacturing data helped rates return back to where they were about a week ago. https://www.mortgagenewsdaily.com/…

MOST HOMES FOR SALE SINCE JULY 2020 – Recent data shows that active inventory and new listings are up significantly year-over-year. https://www.calculatedriskblog.com/…

TURNING CAUTIOUS ON SPENDING – Consumers and businesses are slowing down on the rate of purchases made according to banking data. https://www.cnbc.com/…

CFPB REVIEWING JUNK FEES – The Consumer Financial Protection Bureau (CFPB) is assessing how “junk fees” directly impact the health of consumers. https://www.housingwire.com/…

Investing in real estate has long been considered a smart move for building wealth. Two key reasons for this are the steady home appreciation and the ability to leverage your initial investment. In this blog post, we’ll explore these concepts in detail, showing why real estate remains one of the top ways to build wealth.

Understanding Home Appreciation

Home appreciation refers to the increase in a property’s value over time. Historically, real estate has shown a steady trend of appreciation, making it a reliable long-term investment. Looking at data from the US Census Bureau, homes have appreciated at about 5% annually in the US for the last 40 years.

In our current housing market, demand from homebuyers surpasses the supply in inventory, which have been supportive of home prices and are this trend is expected to keep home values appreciating in the future. At the end of Q1 2024, home prices appreciated by 6.6% year-over-year in the US with the breakdown by state you can see in the chart below.

Lastly, a recent Home Price Expectation Survey by Fannie Mae, which polled over 100 housing experts across the industry, projects an expected increase in home values by 20.8% from Q1 2024 to Q4 2028. This means a home purchased for $750,000 at the beginning of 2024 is expected to rise in value to $906,000 by the end of 2028.

The Power of Leverage in Real Estate Investment

When you purchase a home, you typically provide a down payment and pay closing costs, while the rest of the purchase price is financed through a mortgage. This means you control an asset’s full value with your initial payment, which is considered a form of leverage. As the property appreciates, the return on your investment is calculated based on the property’s entire value and its market exposure, not just your down payment. If we compare this scenario to investing in the stock market, we can see the power of leverage even though the S&P 500 has provided a higher average annual rate of return at about 10%. This leverage magnifies the potential for wealth accumulation through real estate.

Example:

Purchase price: $750,000

Down payment: 5% ($37,500)

Closing costs: $7,500

Total Initial Investment: $45,000

With this initial investment of $45,000, you gain control of a $750,000 asset.

Real Estate Gain:

Total Initial Investment: $45,000 (down payment and closing costs)

Value of Home When Purchased: $750,000

Average Annual Rate of Appreciation: 5% (Home Values Last 40 Years)

After 5 years, the Home Value Increases to: $957,211

5-year Gain in Value: $207,211

Return on Investment (ROI): 460%

Stock Market Gain:

Total Initial Investment: $45,000

Value of Stock When Purchased: $45,000

Average Annual Rate of Return: 10% (S&P 500 Last 30 Years)

After 5 Years, the Stock Value Increases to : $72,473

5-year Gain in Value: $27,473

Return on Investment (ROI): 61%

Homeseed Can Help You Get Started

Discover the possibility of owning a home and investing in real estate with some of our exclusive loan programs that require little to no down payment. This means you can potentially start building equity and wealth with very little upfront investment. Our commitment is to make homeownership accessible and financially advantageous for you. Contact us today to discuss your goals, explore available opportunities, and make informed decisions about your real estate investment.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates have been on a consistent downward trend the last two weeks due to weakening economic data from reports such as the BLS Jobs Report, CPI, and Retail Sales.

With the weaker data, the financial markets are now expecting two rate cuts from the Fed this year.

The next market moving data will likely be the Personal Consumption Expenditures (PCE) report at the end of the month, which is the Fed’s favorite measure of inflation.

Consumer Price Index (CPI)

The Consumer Price Index continues to be the biggest source of momentum for mortgage rates as it measures inflation.

The April report released today showed overall inflation rose 0.3% for the month versus the expected 0.4%, while year-over-year inflation decreased from 3.4% to 3.5%.

Much of the core rate, which excludes food and energy, is coming from motor vehicle insurance (+22.6% YoY) and shelter (+5.7% YoY).

New Home Construction

Housing starts rebounded in April, rising 5.7% from March.

Building permits, which represent future construction, declined.

Completions did rise in April, but the numbers were a bit softer than expected and could limit much-needed supply down the road.

RATES ON A DOWNWARD TREND – Mortgage rates have consistently moved lower the last two weeks after multiple reports showing weakness in the economy. https://www.mortgagenewsdaily.com/…

INFLATION EASES IN APRIL – Today’s CPI report showed inflation in line with expectations and the lowest 12-month core reading since April 2021. https://www.cnbc.com/…

UNLOCKING MORE HOME EQUITY – Freddie Mac, one of the US’s government-sponsored enterprises, is proposing that it be allowed begin purchasing home equity loans which would help unlock equity for homeowners. https://www.businessinsider.com/…

INVESTMENT FROM HUD – The US Department of Housing and Urban Development (HUD) announced it has secured approval for $1.1 billion in funding to help with tribal housing and community development. https://www.housingwire.com/…

Get Started in Less Than 10 Minutes

Get pre-approved with our online mortgage application. It’s simple, fast & secure!